February 2026 Market Views: Two Big Signals for India: The US Trade Deal and Budget FY 2027

In Brief: The February 2026 edition of Market Views highlights a combination of policy-driven tailwinds and near-term market volatility. Some of the key developments include progress on the India–US trade framework, continued government capex support in the Union Budget FY2027, trends in F&O activity post-STT hikes, and a mixed but resilient Q3FY26 earnings picture across market segments. While market performance has seen phases of underperformance versus global peers, historical patterns suggest such periods have often been followed by stabilisation and recovery.

Setting the Context: Markets, Policy, and Data in Focus

In the February 2026 Market Views, Hiren Ved, Director and CIO, Alchemy Capital Management, contextualised recent market movements against a backdrop of significant policy actions, global trade developments, and domestic macro data. Rather than focusing on short-term market reactions, the discussion centred on understanding what the data is signalling, how similar phases have played out historically, and how structural drivers continue to evolve beneath near-term volatility.

India–US Trade Deal: Tariff Comparisons and Relative Positioning

One of the key themes discussed was India’s positioning in the evolving global trade landscape, particularly in comparison to other emerging and developed economies.

US Tariff Rates

As highlighted, India’s tariff positioning sits meaningfully lower than several competing emerging market exporters. This relative positioning becomes important in the context of supply-chain realignment and trade competitiveness, particularly for labour-intensive and export-oriented sectors.

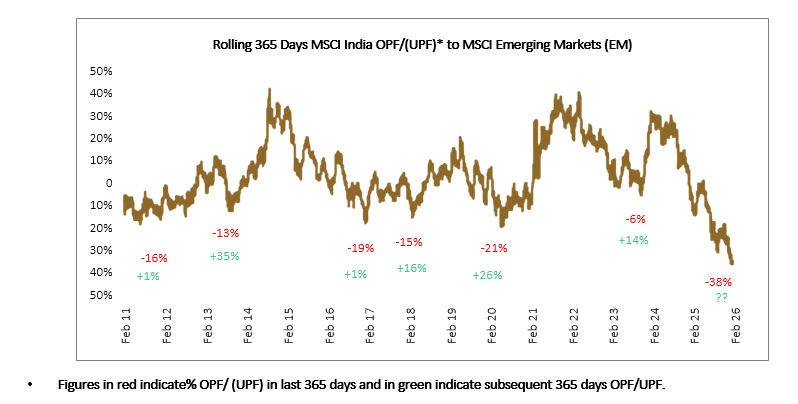

Market Performance Cycles: India vs Emerging Markets

Hiren also addressed concerns around the recent underperformance of Indian equities relative to broader emerging markets (EM) by placing the data in a historical framework.

Rolling 365-Day MSCI India vs MSCI EM Performance

Periods where MSCI India has underperformed MSCI EM have historically been followed by phases of recovery and relative outperformance.

The point emphasised was not prediction, but perspective: relative underperformance phases are not unprecedented, and markets have historically gone through such cycles before normalising.

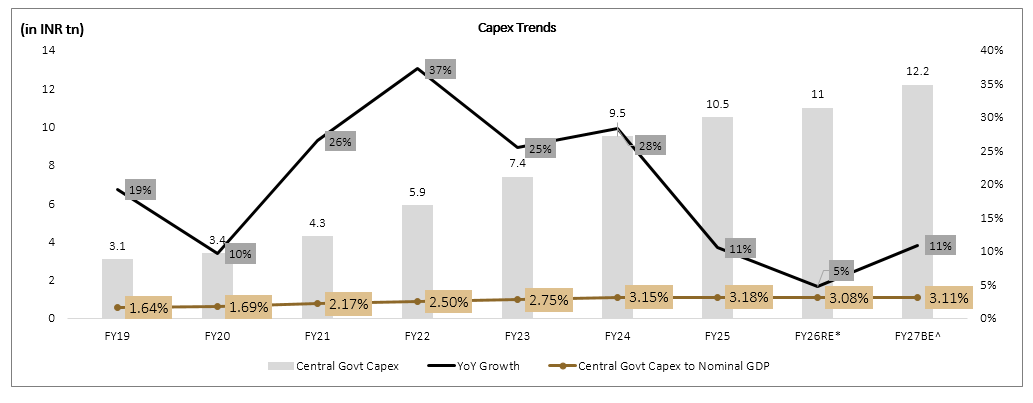

Union Budget FY2027: Capex Remains a Central Pillar

A significant portion of the discussion focused on the Union Budget FY2027, particularly government capital expenditure trends

The commentary underscored the consistency of capex commitment, even as growth rates moderate from very high base levels. Importantly, capex as a percentage of GDP remains elevated, signalling continued focus on infrastructure-led growth.

Where Is the Capex Going? Quality and Composition

Beyond headline numbers, Hiren highlighted the composition of capex spend.

Capex Allocation (INR Bn)

Particulars | FY24 | FY25 | FY26RE | FY27BE | YoY Increase* |

Roads | 2,639 | 2,853 | 2,721 | 2,942 | 8% |

Railways | 2,426 | 2,519 | 2,520 | 2,778 | 10% |

Defence | 1,646 | 1,706 | 1,974 | 2,310 | 17% |

Capex Loans to State | 1,229 | 1,657 | 1,750 | 2,264 | 29% |

Metros | 264 | 315 | 329 | 348 | 6% |

Others | 1,281 | 1,470 | 1,664 | 1,576 | -5% |

Total | 9,485 | 10,520 | 10,958 | 12,218 | 11% |

Roads, railways, and metros continue to account for over half of total capex, while defence emerges as a notable growth area, supported by indigenisation and domestic sourcing initiatives.

Policy Reforms Supporting the Broader Economic Framework

Several structural policy measures were also discussed:

Income tax relief increases disposable incomes

GST rate rationalisation towards a simpler two-rate structure

Labour code implementation is improving workforce flexibility

FDI liberalisation, including the insurance and space sectors

EU–India FTA progress, offering preferential access for exports

Gradual China Engagement

These measures, taken together, were positioned as supportive of medium-term growth rather than immediate market triggers.

F&O Markets and STT (Securities Transaction Tax):

Hiren addressed concerns around higher STT and its impact on derivatives activity.

F&O Volumes Have Continued to Rise Historically Despite Higher Securities Transaction Tax (STT)

Effective Date | Instrument/Transaction | Old STT Rate | New STT Rate | Change in STT | Growth* in ADTO^ Options After STT Hike | Growth* in ADTO Futures After STT Hike |

1st April, 2023 | Futures (Sale) | 0.0100% | 0.0125% | 0.0025% | 32.7% | 15.3% |

1st April, 2023 | Options (Sale on Premium) | 0.0500% | 0.0625% | 0.0125% | 32.7% | 15.3% |

1st October, 2024 | Futures (Sale) | 0.0125% | 0.0200% | 0.0075% | -11.3% | -10.6% |

1st October, 2024 | Options (Sale on Premium) | 0.0625% | 0.1000% | 0.0375% | -11.3% | -10.6% |

1st April, 2026 | Futures (Sale) | 0.0200% | 0.0500% | 0.0300% | ? | ? |

1st April, 2026 | Options (Sale on Premium) | 0.1000% | 0.1500% | 0.0500% | ? | ? |

1st April, 2026 | Options (Exercise - intrinsic value) | 0.1250% | 0.1500% | 0.0250% | ? | ? |

The key takeaway was that STT hikes are not new, and previous increases have seen mixed short-term impact but did not structurally impair market participation over time.

Q3FY26 Earnings: Growth with Divergence

Earnings data formed another important anchor.

While margins moderated marginally, earnings growth remained positive across a broad base of companies.

Market Cap Segments: Large, Mid, Smallcaps

Largecaps showed steady revenue growth with stable margins

Midcaps delivered double-digit revenue growth but faced margin pressure

Smallcaps recorded healthy profit growth, albeit with higher volatility

This divergence was positioned as a reflection of differing base effects and cost dynamics rather than a uniform slowdown.

Putting It All Together: Data Over Noise

The February 2026 Market Views reinforced a recurring theme: markets move in cycles, but data provides context. Trade developments, fiscal policy continuity, and earnings resilience together paint a picture that is more nuanced.

Rather than reacting to individual data points, the emphasis remained on understanding trends, historical patterns, and structural drivers shaping India’s economic trajectory.

Closing Perspective

As highlighted above, India’s macro and policy framework continues to evolve with a long-term orientation, even as markets navigate phases of uncertainty. By grounding market views in data and historical context, investors are better positioned to interpret developments beyond short-term fluctuations.

Disclaimers:

This blog is for informational purposes only and should not be considered an offer or solicitation to buy or sell any securities or make any investments. We recommend readers take independent advice before making any investment decisions. Please refer to our Disclaimer and Disclosures for more details.

General Risk Factors:

All products / investment approach attract various kinds of risks. Please read the relevant Disclosure Document/ Client Agreement/ Offer Documents (includes Private Placement Memorandum and Contribution Agreement) carefully before investing.

General Disclaimers:

The information and opinions contained in this report/ presentation have been obtained from sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete.

Information and opinions contained in the report/ presentation are disseminated for the information of authorized recipients only and are not to be relied upon as advisory or authoritative or taken in substitution for the exercise of due diligence and judgement by any recipient.

The information and opinions are not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments.

Nothing contained herein, including past performance, shall constitute any representation or warranty as to future performance.

The client is solely responsible for consulting his/her/its own independent advisors as to the legal, tax, accounting and related matters concerning investments and nothing in this document or in any communication shall constitutes such advice.

The client is expected to understand the risk factors associated with investment & act on the information solely on his/her/its own risk. As a condition for providing this information, the client agrees that Alchemy Capital Management Pvt. Ltd., its Group or affiliates makes no representation and shall have no liability in any way arising to them or any other entity for any loss or damage, direct or indirect, arising from the use of this information.

This document and its contents are proprietary information of Alchemy Capital Management Pvt. Ltd and may not be reproduced or otherwise disseminated in whole or in part without the written consent.

The information and opinions contained in this document may contain “forward-looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “seek”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, including those set forth under the Disclosure Document/Offer Documents, actual events or results or the actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Regulatory Disclosures:

All clients have an option to invest in the above products / investment approach directly, without intermediation of persons engaged in distribution services.

This document, its contents, especially the Performance related information, is not verified by SEBI or any regulator.

Take The

Next Step

Explore how Alpha 100 can fit into your long-term allocation framework.